Overview

The current state of carbon pricing clearly reflects the gap between policies and pledges. While carbon prices reached record highs across a number of ETSs and carbon taxes over the past year, the majority of carbon prices remain significantly below what is needed to meet the goals of the Paris Agreement. Greater carbon pricing ambition can play a crucial role in closing the pledge-policy gap when part of a comprehensive climate policy package and grounded in robust long-term strategies. An increasing interest in cross-border approaches to carbon pricing reflects attempts to realize domestic climate ambition while addressing concerns related to international competitiveness and carbon leakage.

Adopting ambitious carbon prices remains politically challenging, particularly in the context of rising energy commodity prices and continued pressure on economies from the ongoing COVID-19 pandemic. Implementing and maintaining carbon pricing in this context requires a strong emphasis on ensuring carbon pricing is fair, inclusive, and well communicated. At the same time, high energy commodity prices coupled with current geopolitical tensions may also provide an additional incentive for governments to speed up their transition to alternative energy sources. Moreover, recent research highlights that environmental taxes can be less distortionary than other taxes, particularly in times of economic recovery.

The private sector, meanwhile, has seen a sharp rise in voluntary mitigation targets, many of which rely to at least some extent on using carbon credits. This has contributed to record issuances, trades, and prices, though it has also triggered increased scrutiny. A growing number of initiatives are emerging to assess ambition in voluntary pledges and carbon credit quality. In addition, international carbon market rules agreed at COP26 provide flexibility to countries to authorize international transfers of credits from voluntary carbon projects. Host countries that opt to require such authorization will in turn apply a corresponding adjustment for such transfers, which must be reflected in their NDC reporting emissions balance. These factors are likely to lead to increasing heterogeneity in the voluntary carbon market as buyers place different values on host country authorization as well as credit quality. The adoption of international carbon market rules also provides a framework for greater intergovernmental carbon trading, although the potential demand for such trading is uncertain.

Carbon taxes and emissions trading systems

Carbon pricing can provide the impetus for economic transformation and recovery

- More ambitious carbon prices can help close the gap between pledges and policy and “keep 1.5 alive.”

- Along with lowering emissions, carbon pricing can improve energy and industrial efficiency, limit reliance on imported energy, promote cleaner air, protect and regenerate landscapes, and provide a valuable source of government revenue.

- But adopting carbon prices remains politically challenging, particularly amid rising inflation and energy prices. There is a clear need to ensure policies are fair, effective, and embedded within integrated climate and social policies.

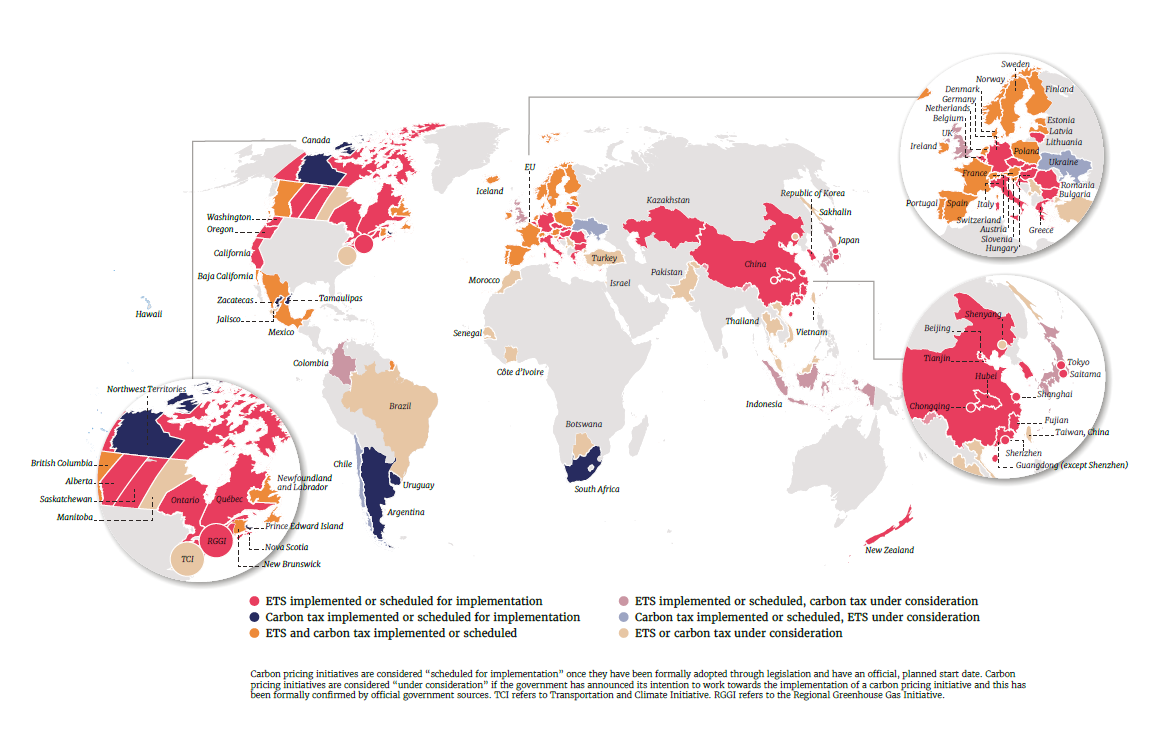

Direct carbon pricing continues to be adopted but global coverage remains low

- Worldwide, 68 carbon pricing instruments (CPIs), including taxes and emissions trading systems (ETSs), are operating and two more are scheduled for implementation.

- CPIs in operation cover approximately 23% of total global greenhouse gas (GHG) emissions. This represents a small increase in total global coverage as a result of four new systems commencing in the past year.

- The International Maritime Organization is considering placing a price on emissions from international shipping activities. If adopted, this would represent a major step in tackling global GHG emissions.

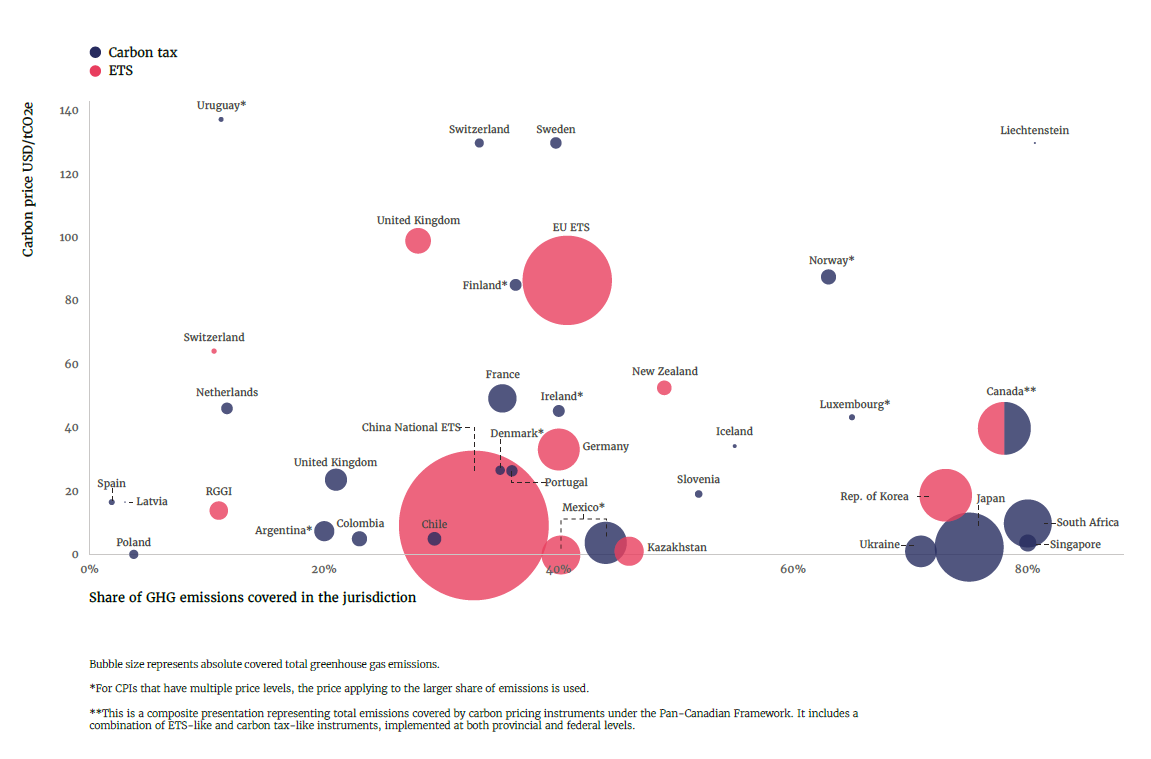

Carbon prices have hit record highs in many jurisdictions

- Record ETS prices were observed in the European Union (EU), California, New Zealand, and Republic of Korea, among other markets, while several carbon taxes also saw prices hit their highest levels yet.

- A combination of policy reforms, anticipated changes, speculative investment interest, and broader economic trends, especially in global energy commodity markets, are driving these ETS price spikes.

- Nonetheless, prices must rise considerably more to meet the Paris Agreement temperature goals, as less than 4% of global emissions are currently covered by a direct carbon price within the range needed by 2030.

Figure 1. Map of carbon taxes and ETSs (2022)

Figure 2 Absolute emissions coverage, share of emissions covered, and prices per jurisdiction

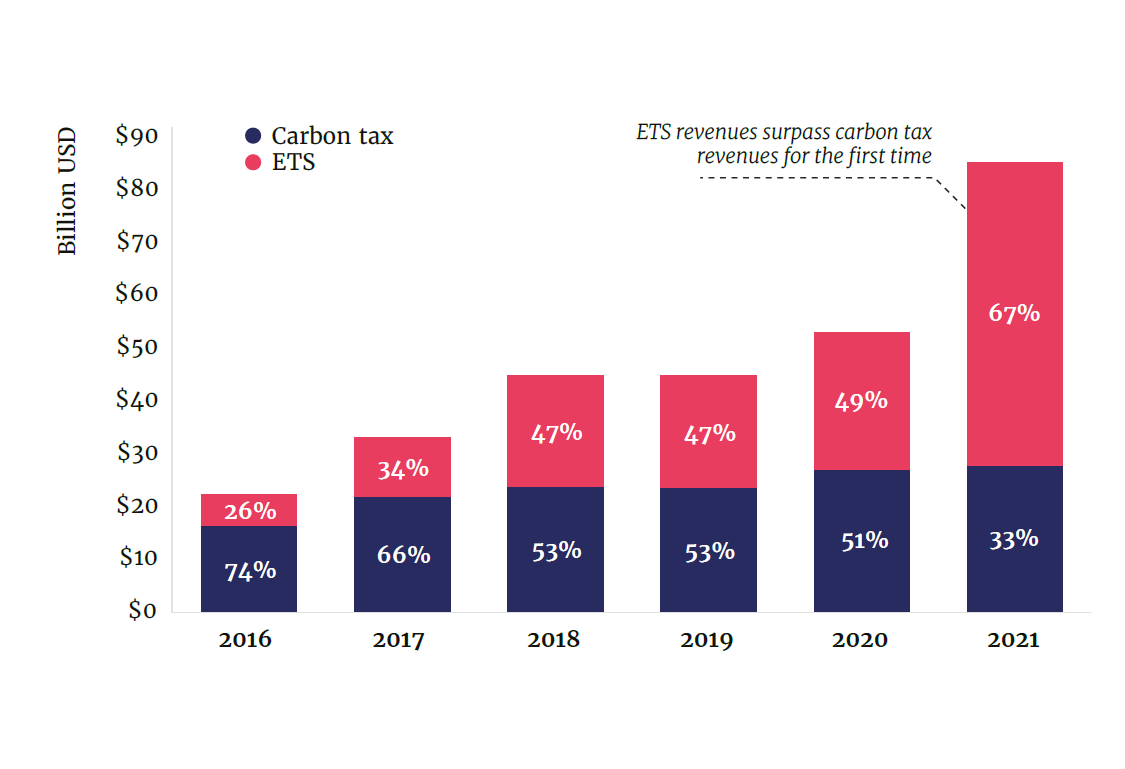

Carbon revenues have increased sharply

- Global carbon pricing revenue increased by almost 60% to around USD 84 billion.

- With prices rising and reduced free allocation, ETS revenues surpassed carbon tax revenues for the first time.

- Increasing carbon pricing revenues can support sustainable economic recovery, finance broader fiscal reforms, or help buffer countries from economic and international turbulence.

Figure 3 Evolution of global carbon pricing revenues over time

Cross-border approaches to carbon pricing are increasingly gaining traction

- The EU moved closer to adopting its carbon border adjustment mechanism, and Canada and the United Kingdom (UK) are exploring options for similar mechanisms.

- The International Monetary Fund (IMF) and World Trade Organization (WTO) are advocating for an international carbon pricing floor.

- Some countries have moved toward the adoption of international climate clubs, including the proposed United States (US)-EU Carbon-Based Sectoral Arrangement on Steel and Aluminum Trade.

- These approaches can fortify domestic support, prevent carbon leakage, and encourage mitigation beyond national borders.

Carbon crediting - markets and mechanisms

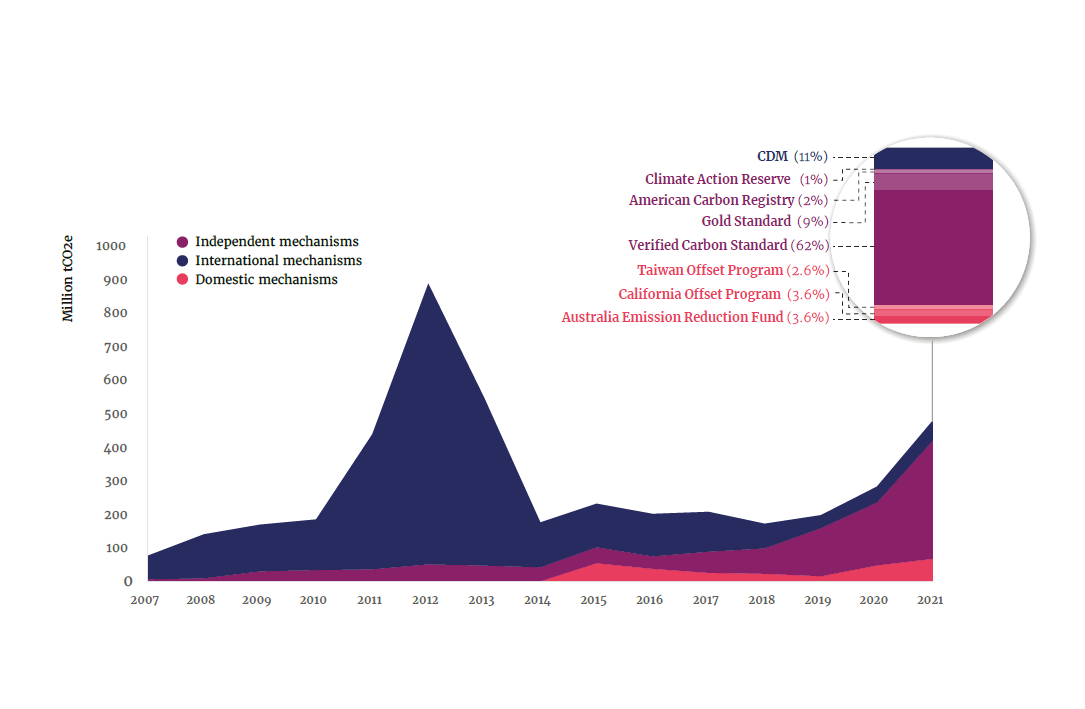

Markets for carbon credits are growing rapidly

- Credits from independent crediting mechanisms clearly dominate the carbon market.

- Annual voluntary carbon market value exceeded USD 1 billion for the first time, driven by corporate commitments.

- Compliance demand for carbon credits remains limited, though new rules for international carbon markets under Article 6 of the Paris Agreement provide clarity that may enable future growth.

Figure 4 Global volume of issuances per category of mechanism (2007-2021)

Diverse purchaser preferences make market growth uneven

- Nature-based credits are in especially high demand: forestry and land use transactions more than doubled between 2020 and 2021.

- Increasing demand for carbon removals has resulted in price increases for these credits.

- The voluntary carbon market continues to be strongly diverse, with purchasers placing widely different values on characteristics such as sector, geography, and perceived co-benefits.

New financial services, technologies and governance frameworks are shaping carbon markets

- Financial actors are becoming more active in the carbon market, while blockchain has enabled a new wave of decentralized financial innovations that show the technology’s potential but have reignited some longstanding concerns about transparency and quality.

- Diverse governance frameworks are emerging from stakeholders and institutions that aim to address concerns regarding the integrity of carbon credits and how companies use them.

- New rules on Article 6 increase certainty while also adding complexity to carbon credit markets and may lead to increasingly divergent approaches emerging across actors and geographies.